Digital Nomad Tax Comparison 2026: 7 Countries Head-to-Head

Spain vs Portugal vs Thailand vs Croatia vs UAE vs Greece vs Malaysia. Which country leaves the most money in your pocket?

I've lived in 4 of these 7 countries and done the tax math for all of them. The "best" country depends almost entirely on your income level, your work structure (employee vs freelancer), and what you value beyond tax rates. Let me walk you through the actual numbers at three income levels: $30,000, $80,000, and $200,000.

How I Calculated These Numbers

Every figure below includes:

- Income tax at 2026 rates (including surtaxes, solidarity contributions)

- Social security contributions (the actual minimum/mandatory amounts)

- Standard deductions and allowances where applicable

Numbers don't include: private health insurance costs, visa fees, accounting costs. Those add $800-3,000/year depending on the country. I've noted major caveats in the country-specific section.

Currencies: I'm using USD as the base, converting at mid-2026 approximate rates. Local currencies fluctuate — run the numbers at current rates before deciding.

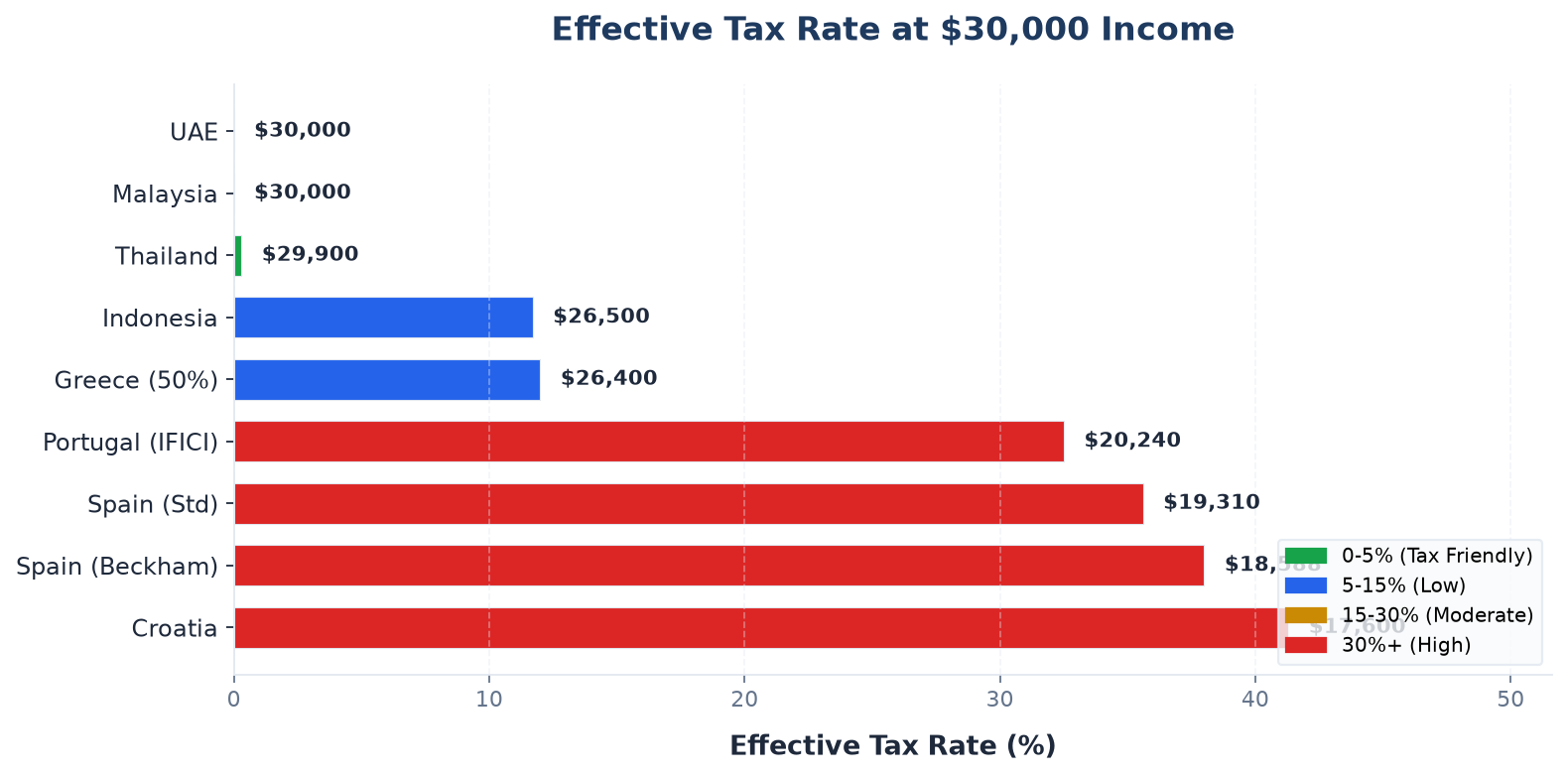

At $30,000 Income: The Budget Nomad

If you're earning $30,000 (about €27,800), taxes matter less than cost of living and visa accessibility. Here's the breakdown:

| Country | Income Tax | Social Security | Total Burden | Take-Home | Effective Rate |

|---|---|---|---|---|---|

| UAE | $0 | $0 (freelancer) | $0 | $30,000 | 0% |

| Thailand | $0* | $100 | $100 | $29,900 | 0.3% |

| Malaysia** | $0 | $0 | $0 | $30,000 | 0% |

| Indonesia | $2,800 | $700 | $3,500 | $26,500 | 11.7% |

| Spain (Beckham) | $6,672 | $4,740 | $11,412 | $18,588 | 38.0% |

| Spain (progressive) | $5,950 | $4,740 | $10,690 | $19,310 | 35.6% |

| Portugal (IFICI) | $5,560 | $4,200 | $9,760 | $20,240 | 32.5% |

| Croatia (Split) | $6,400 | $6,000 | $12,400 | $17,600 | 41.3% |

| Greece (50% reduction) | $1,800 | $1,800 | $3,600 | $26,400 | 12.0% |

*Thailand: at $30K, you're under the taxable threshold once deductions apply **Malaysia: included as an additional comparison country

The clear winners at $30,000: UAE, Thailand, Malaysia — all near-zero. Greece with the 50% reduction is the only EU option that keeps your effective rate under 15%.

Spain at $30K is actively bad. The Beckham Law flat 24% is actually worse than standard progressive at this income level — one of the few income points where standard rates beat Beckham. Portugal's IFICI 20% flat doesn't help much either at this level.

But here's the thing about $30,000: the countries with zero tax have visa barriers. UAE requires $42,000/year income for the remote work visa. You can't legally live in the UAE at $30,000. Thailand's DTV requires ฿500,000 ($14,000) in savings, which you might manage, but DTV holders at $30K income often face extra scrutiny at immigration.

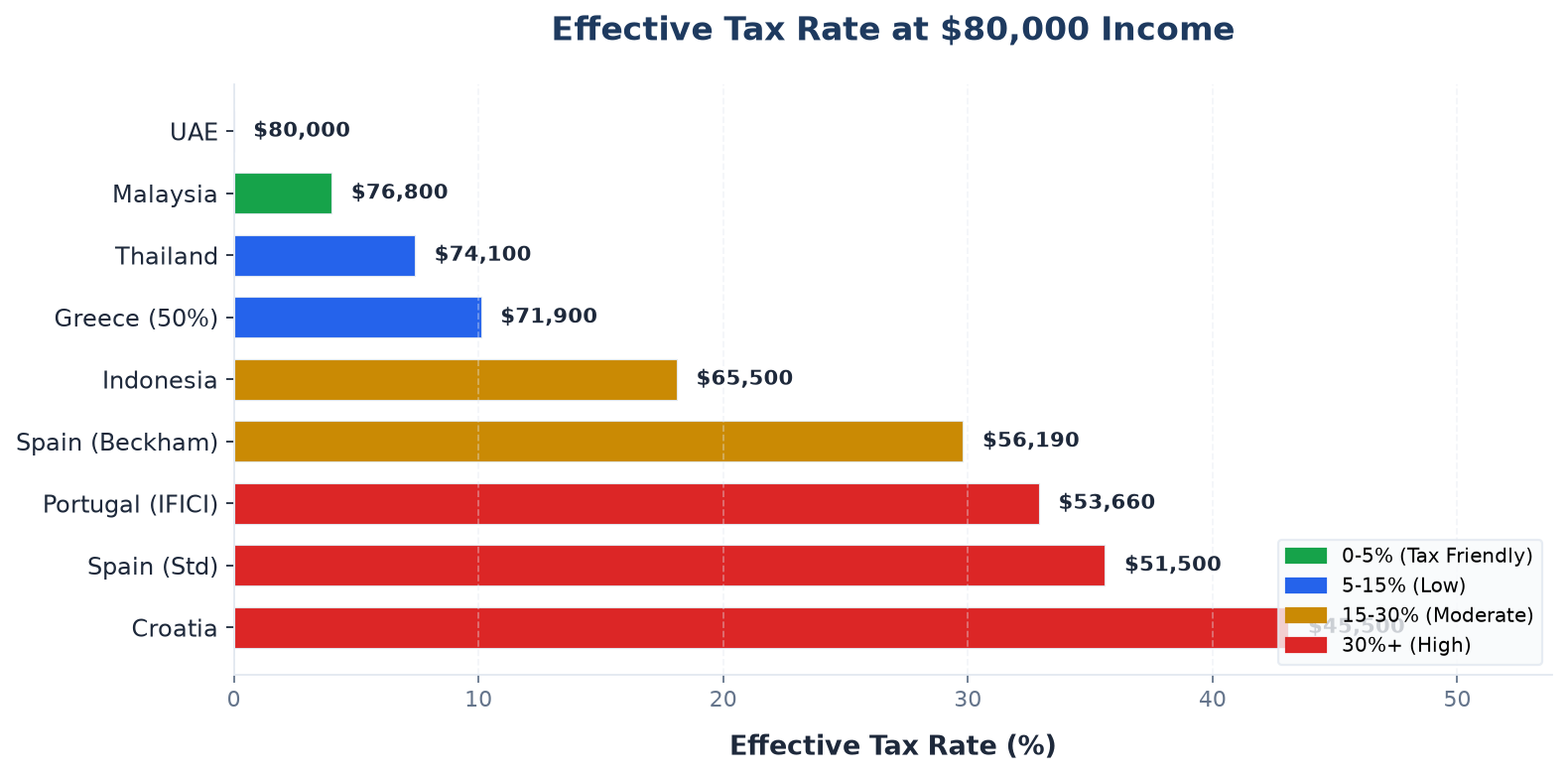

At $80,000 Income: The Sweet Spot

This is where tax optimization actually matters. At $80,000 (€74,200), you're paying real money in taxes and the differences between countries are stark:

| Country | Income Tax | Social Security | Total Burden | Take-Home | Effective Rate |

|---|---|---|---|---|---|

| UAE | $0 | $0 | $0 | $80,000 | 0% |

| Thailand | $5,800 | $100 | $5,900 | $74,100 | 7.4% |

| Malaysia | $3,200 | $0 | $3,200 | $76,800 | 4.0% |

| Indonesia | $13,000 | $1,500 | $14,500 | $65,500 | 18.1% |

| Spain (Beckham) | $17,810 | $6,000 | $23,810 | $56,190 | 29.8% |

| Spain (progressive) | $22,500 | $6,000 | $28,500 | $51,500 | 35.6% |

| Portugal (IFICI) | $14,840 | $11,500 | $26,340 | $53,660 | 32.9% |

| Croatia (Split) | $18,500 | $16,000 | $34,500 | $45,500 | 43.1% |

| Greece (50% red.) | $4,500 | $3,600 | $8,100 | $71,900 | 10.1% |

Thailand and Malaysia remain incredibly efficient. UAE is still zero. Greece with the 50% reduction jumps out as the best EU option.

Croatia becomes painful — 43.1% effective rate because the social security burden hits hard and the 30% bracket kicks in above €50,400. Portugal looks worse than Spain with the Beckham Law because social security at 21.4% on 70% of income adds approximately €10,000+.

Important note on Portugal: The IFICI 20% flat applies only to qualifying work activities. If you're a marketing strategist making $80,000 and your activity doesn't qualify, you're on standard progressive rates which would push your effective rate to about 38% — worse than Spain Beckham.

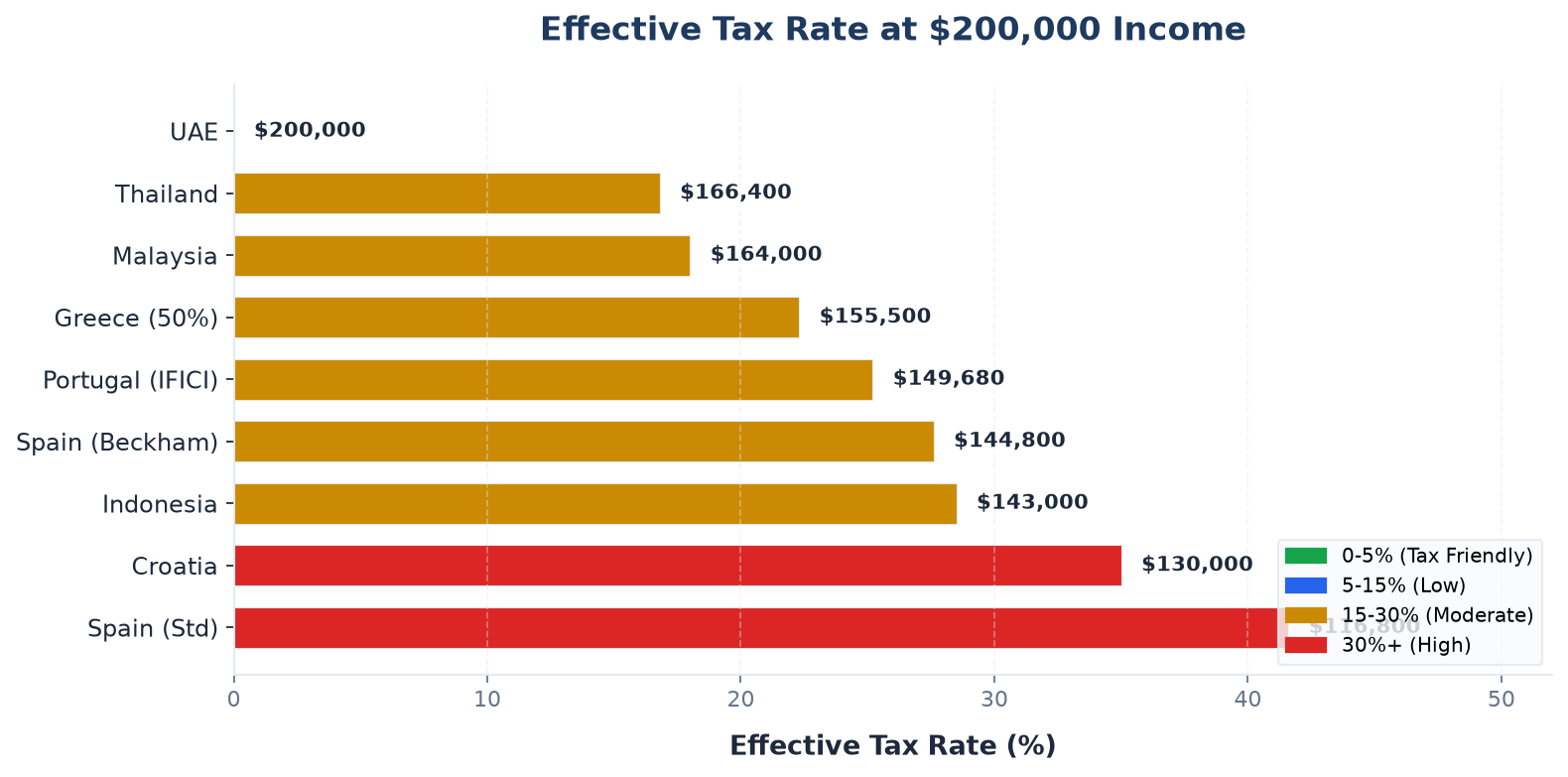

At $200,000 Income: High Earners

At this level, tax minimization is a significant financial decision. A 10% rate difference is $20,000/year:

| Country | Income Tax | Social Security | Total Burden | Take-Home | Effective Rate |

|---|---|---|---|---|---|

| UAE | $0 | $0 | $0 | $200,000 | 0% |

| Thailand | $33,500 | $100 | $33,600 | $166,400 | 16.8% |

| Malaysia | $36,000 | $0 | $36,000 | $164,000 | 18.0% |

| Indonesia | $55,000 | $2,000 | $57,000 | $143,000 | 28.5% |

| Spain (Beckham) | $48,000 | $7,200 | $55,200 | $144,800 | 27.6% |

| Spain (progressive) | $76,000 | $7,200 | $83,200 | $116,800 | 41.6% |

| Portugal (IFICI) | $37,120 | $13,200 | $50,320 | $149,680 | 25.2% |

| Croatia (Split) | $54,000 | $16,000 | $70,000 | $130,000 | 35.0% |

| Greece (50% red.) | $38,000 | $6,500 | $44,500 | $155,500 | 22.3% |

A few patterns emerge. Spain's Beckham Law stays at 24% flat through $200,000 (the 47% surcharge above €600,000 doesn't apply). Portugal's IFICI holds at 20% flat. Both provide predictability that Thailand's progressive system can't match — Thailand's effective rate climbs from 9.4% at $80K to 16.8% at $200K.

UAE is the mathematical winner at every income level. If your only goal is minimizing tax, and you can genuinely break home-country tax residency, the UAE is unbeatable. Most people can't or don't want to live there year-round — the gap between mathematical optimum and actual life quality is real.

The Social Security Surprise

One thing that jumps out: social security contributions vary from $100/year (Thailand) to $16,000/year (Croatia). That's a $15,900 difference on the same income.

European countries justify this with public services — healthcare, pension systems, unemployment benefits — and if you plan to stay long-term, those systems have value. Croatia's universal healthcare and eventual pension access are worth something, though quantifying "something" is personal.

But for a digital nomad who might stay 2-3 years and move on, those contributions are largely wasted. You won't vest in the pension. You might use the healthcare a few times. The cost-benefit is poor for short-term residents.

This is where Southeast Asia and the UAE shine. Low social security contributions mean you keep more income and buy private services directly. Private health insurance in Thailand costs $600-1,200/year. Even adding that to the tax total, Thailand stays far cheaper than any European option.

Quantitative Rankings at Each Income Level

At $30,000:

- UAE / Thailand / Malaysia (near-zero)

- Greece 50% reduction (12%)

- Indonesia (11.7%)

- Portugal standard (20.9%)

- Spain standard (35.6%)

At $80,000:

- UAE (0%)

- Malaysia (4.0%)

- Thailand (7.4%)

- Greece 50% reduction (10.1%)

- Indonesia (18.1%)

- Spain Beckham (29.8%)

- Portugal IFICI (32.9%)

- Spain progressive (35.6%)

- Croatia (43.1%)

At $200,000:

- UAE (0%)

- Thailand (16.8%)

- Malaysia (18.0%)

- Greece (22.3%)

- Portugal IFICI (25.2%)

- Spain Beckham (27.6%)

- Indonesia (28.5%)

- Croatia (35.0%)

- Spain progressive (41.6%)

Beyond Tax: What the Numbers Don't Show

Thailand's DTV visa is flexible, cheap, and gives you 5-year access. The tax system is gentle. But internet outages happen, burning season in Chiang Mai is February-April, and the long-term political situation is uncertain. These aren't spreadsheet lines but they affect your daily life.

Portugal has the most developed digital nomad infrastructure in Europe. The D8 visa process is well-documented, banking is modern, and Lisbon's tech scene is genuinely world-class. You pay for this through higher social security and living costs.

Spain offers incredible quality of life — weather, food, culture, health infrastructure — and the Beckham Law makes it affordable at higher incomes. But Spanish bureaucracy is legendary for being slow and confusing. Budget 30-40% of your energy for administrative tasks in your first year.

Greece's 50% reduction is mathematically brilliant but the bureaucracy wears on you. The AADE online platform has improved but still breaks in creative ways. If you have patience for administrative friction, Greece delivers European lifestyle at Asian-competitive tax rates for 7 years.

UAE is the tax king but requires genuine commitment: breaking home-country residency, handling summer heat, navigating a culture that's conservative by Western standards. The people who thrive there have clear professional or lifestyle reasons beyond tax.

Which Country Wins?

Best for $30K-50K: Thailand or Malaysia. Taxes near zero, cost of living is low, visa requirements are achievable. If you want Europe, Greece with the 50% reduction is the only competitive option.

Best for $50K-120K: Greece 50% reduction for the first 7 years. After that, Portugal IFICI if you qualify, or Spain Beckham Law if you're employed by a foreign company. Thailand remains competitive but the tax gap narrows.

Best for $120K+: UAE if you can handle it. Spain Beckham Law or Portugal IFICI if you want Europe. The European options cost $25,000-40,000 more in taxes but deliver infrastructure, healthcare, and Schengen mobility that the UAE doesn't match.

Best overall flexibility: Thailand. The DTV gives you 5-year access with low tax obligations, Southeast Asia's best infrastructure, and proximity to the rest of Asia. It's not the mathematically optimal choice at every income level, but it's the most practical for the most people.

I say this having paid taxes in 4 different countries over the past 5 years: the best tax strategy is the one you can actually execute without constant stress. A zero-tax setup you're always worried about losing is worse than a 15% setup you never think about.

Related Articles

Digital Nomad Taxes: A Beginners Guide (2026)

Everything you need to know about managing taxes as a digital nomad — residency, double taxation, and the countries that make it easiest.

7 Tax Mistakes Digital Nomads Make (And How to Avoid Them)

From wrong residency assumptions to missing deadlines — these are the tax traps that cost nomads thousands every year.